Bank Credit Card Offers Singapore

Best Bank Credit Card Offers: Top Deals & Rewards 2025

A cashback credit card allows you to earn back a percentage of what you spend, making every purchase more rewarding. Whether you’re shopping for groceries, dining out or booking travel, the right card helps you to save money effortlessly.

With so many options available, choosing the best cash back credit card Singapore can feel overwhelming. Some cards offer flat-rate cashback while others provide higher rewards on specific spending categories like fuel, dining or online shopping.

Understanding how these cards work can help you maximise savings and choose the one that fits your lifestyle best. This guide breaks down the top cashback credit cards in Singapore, how they work and tips to get the most out of your cashback rewards.

A cashback credit card in singapore returns part of the money you spend. Instead of collecting points, you save real cash that gets added to your account.

There are three kinds of cashback cards:

Pick the right one based on how you spend money.

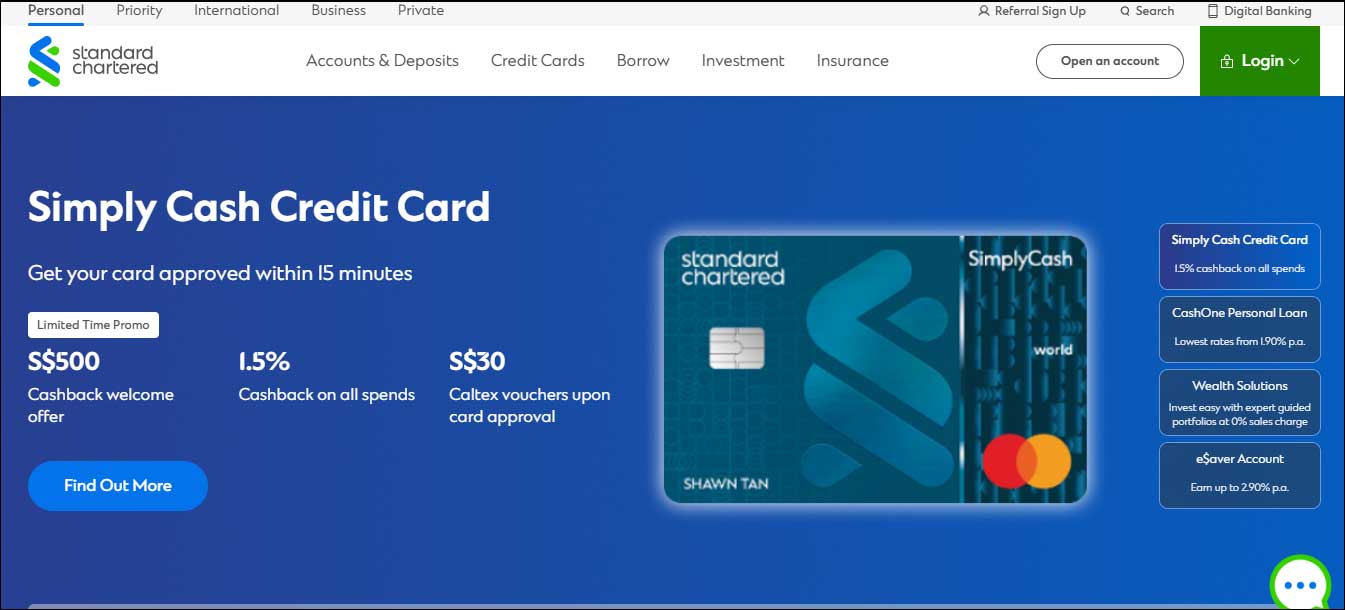

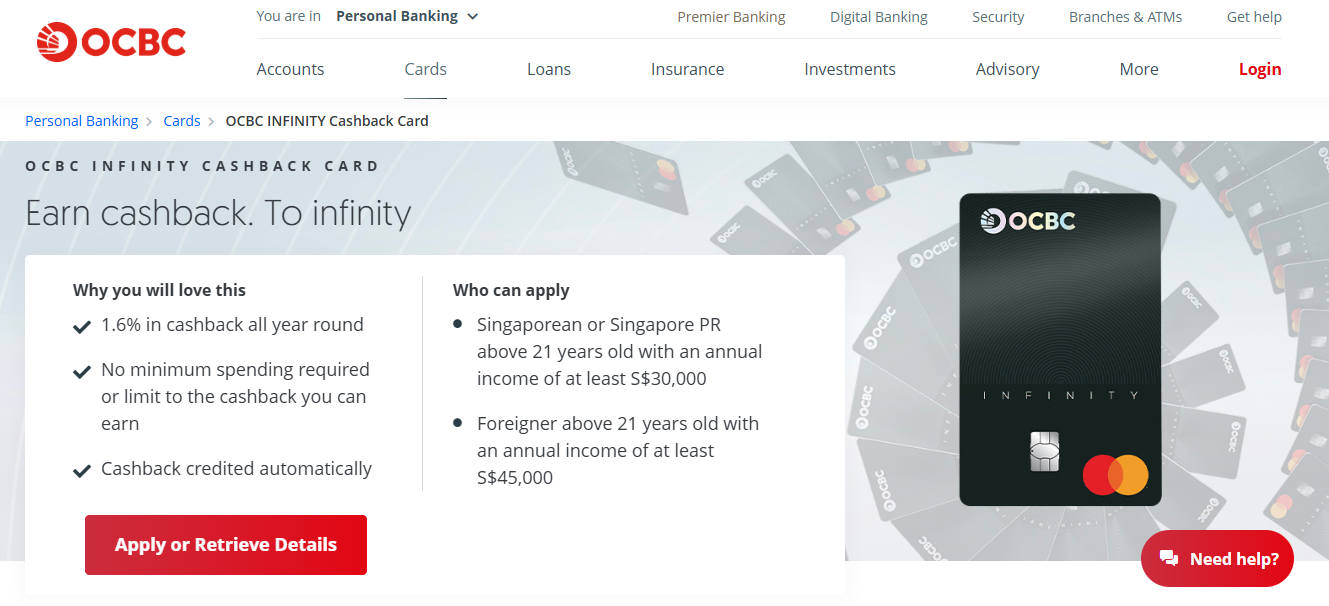

This is a trouble-free cashback credit card Singapore that offers 1.5% unlimited cashback on all purchases, which makes it an excellent choice for those who prefer simplicity. With no minimum spending required and no category restrictions, cardholders enjoy steady cashback without worrying about spending habits.

A no-fuss cashback card with 1.5% unlimited cashback on all purchases. No need to track categories or spending limits.

|

For those looking for higher flat-rate cashback, this card offers 1.6% unlimited cashback on all transactions. Like the Standard Chartered Simply Cash, it has no minimum spending and comes with an annual fee of $196.20. It’s ideal for people who spend across multiple categories and prefer a higher fixed cashback rate without tracking specific purchases.

With 1.6% unlimited cashback, this card is slightly better than Standard Chartered Simply Cash. If you spend across different categories, it ensures a steady return on every purchase.

|

This card rewards food lovers and frequent travelers with 8% cashback on dining, entertainment, and travel. However, to enjoy these high rewards, cardholders must meet the minimum spending of $600 per month. The annual fee is $196.20, but the significant savings on dining out and travel bookings make this card an attractive choice for those who enjoy these activities regularly.

Perfect for food lovers and travellers. This card fills your pockets with extra savings when you dine out or book trips.

|

It offers one of the highest cashback rates in Singapore, this card provides up to 20% cashback on selected categories such as groceries, fuel, and utility bills. However, cashback rates vary depending on spending tiers ($500, $1,000, or $2,000 per month). With an annual fee of $196.20, this is the best cash back credit card Singapore for those who plan their expenses strategically to maximise rewards.

One of the highest cashback cards in Singapore. If you spend wisely, you score big savings on groceries, fuel, and bills

|

An all-rounder cashback credit card in Singapore, this card provides up to 6% cashback on everyday expenses like dining, groceries, transport, and utilities. A minimum spend of $800 per month is required to unlock the highest rates. With an annual fee of $192.60, this card is great for families and individuals looking for consistent savings on daily expenses.

A great everyday cashback card. Slash your bills while shopping for food, taking the bus, or paying for household services

|

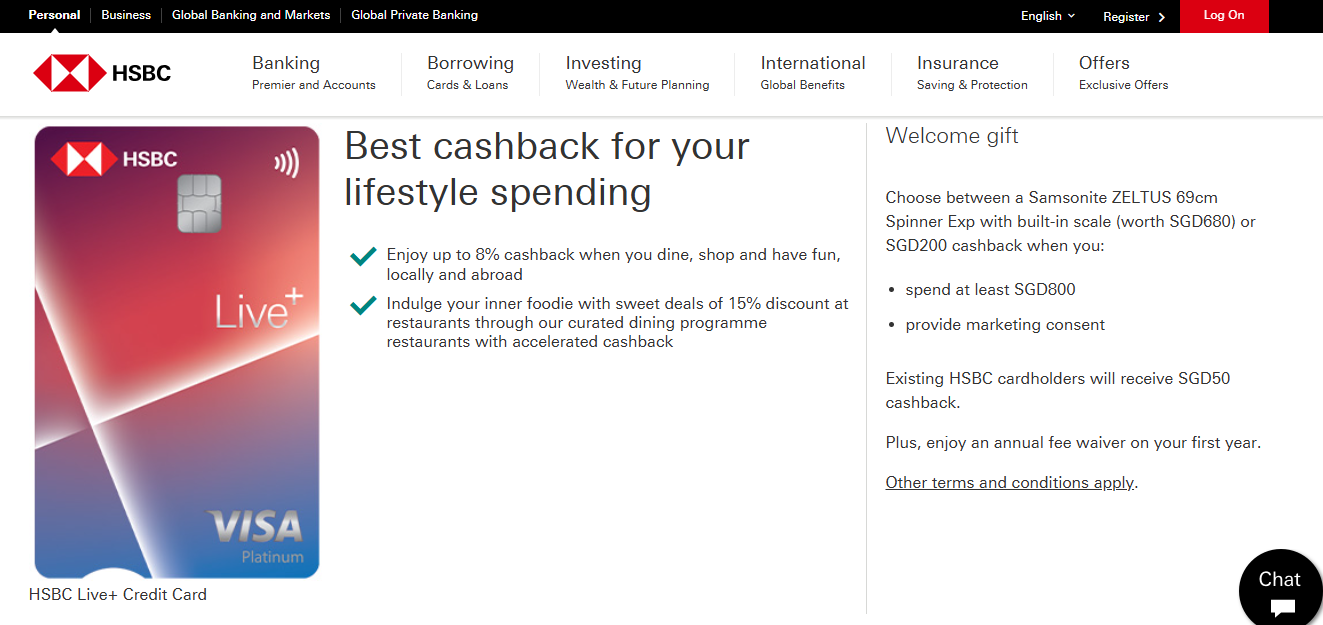

Designed for big spenders, this card offers up to 3.5% cashback on all spending, making it a great choice for those who regularly make large purchases. However, to enjoy the maximum cashback, cardholders must meet a minimum spending of $2,000 per month. The best part? It’s free for HSBC Advance customers, making it a cost-effective choice for loyal HSBC users.

This card is created for big spenders, and it offers up to 3.5% cashback on all spending. It is best suited for those who frequently make large purchases and want consistent returns.

|

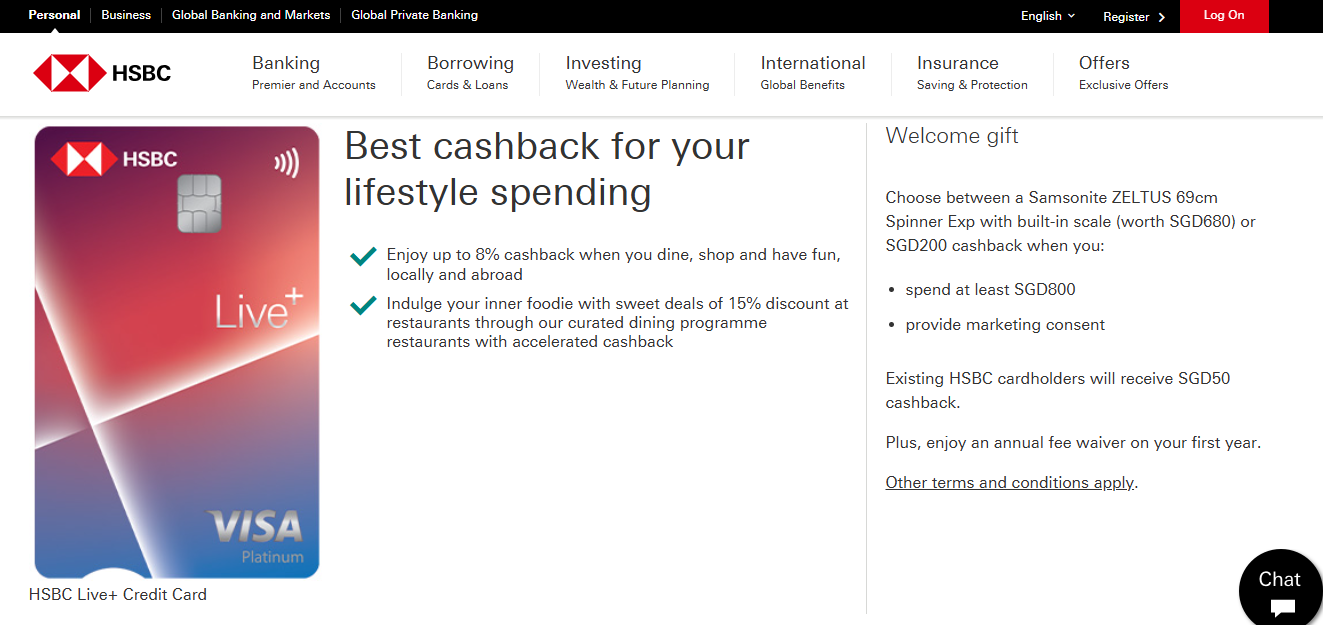

A favorite among families and foodies, this card offers 8% cashback on dining, groceries, and petrol. The minimum spending requirement is $800 per month, and the annual fee is $196.20. If you regularly dine out or shop for groceries, this card provides excellent savings opportunities.

Great for families and foodies who enjoy strong cashback on groceries and dining. If you spend heavily on essentials, this card helps you save significantly.

|

One of the few cashback cards with no annual fee, this card provides up to 10% cashback on selected categories like dining, travel, and online shopping. A minimum spend of $800 per month is required. If you are looking for a high-reward, no-fee card, this is a fantastic option.

A high-reward cashback card with no annual fee on dining, travel and online shopping. A great choice for frequent travelers and shoppers.

|

A great unlimited cashback card, it offers 1.7% cashback on all purchases, which is higher than most flat-rate cashback cards. With no minimum spending, it’s a good choice for those who want a steady cashback return without restrictions. However, the annual fee is $196.20.

Higher than most flat-rate cashback cards. This one guarantees a steady return on every purchase.

|

This easy-to-use cashback credit card in Singapore provides 1.5% unlimited cashback on all purchases. A key benefit is that first-time users get extra rewards, making it appealing for those new to cashback cards. With no minimum spend and an annual fee of $174.40, it’s a solid all-purpose option.

This is a straightforward cashback card that rewards every purchase. Plus, it offers extra rewards for first-time users, making it an attractive choice for new cardholders.

|

It offers 1.6% unlimited cashback, This card is perfect for those who want steady savings without tracking spending categories. With no minimum spending and an annual fee of $196.20, it’s a straightforward cashback card for everyday spending.

Ideal for those who want steady cashback without tracking spending categories. With 1.6% unlimited cashback, this card offers simple, stress-free savings.

|

An excellent choice for frequent online shoppers and diners, this card provides up to 10% cashback on online shopping and dining. The minimum spend is $800 per month, and the best part? No annual fee. If you shop online often, this card helps you save significantly.

Perfect for frequent online shoppers and diners because this card offers up to 10% cashback on both. The no-annual fee makes it a cost-effective option.

|

It is designed for commuters, this card offers 0.3% cashback on all spending, with a minimum spend of $500 per month. It’s great for those who use public transport daily and want to maximise their transport savings. The annual fee is $196.20.

This card is best for commuters, this card provides extra perks on transport spending, making it a great choice for those who rely on public transport daily.

|

Perfect for frequent shoppers at Yuu merchants like 7-Eleven and Cold Storage, this card provides up to 18% cashback. There’s no minimum spend, but the annual fee is $196.20. If you regularly shop at these stores, this card offers significant savings.

Ideal for frequent shoppers at Yuu partner stores, such as 7-Eleven and Cold Storage by offering up to 18% cashback. A great way to maximise rewards on daily essentials.

|

Some cards demand a certain spending level before unlocking full cashback. If you don’t reach it, you miss out on savings.

Many cards cap cashback earnings. If you spend a lot, pick an unlimited cashback card instead.

If you’re looking for the best credit card cash bonus, compare the latest offers and promotions to maximise your savings.

Finding the best cashback credit card in Singapore depends on your lifestyle and spending habits. If you prefer a simple, hassle-free option, the Standard Chartered Simply Cash Credit Card is a great choice.

For those who spend heavily on food and fuel, the Citi Cash Back Card provides excellent savings. If maximising cashback is your priority, the UOB One Card stands out with its high rebate rates. Choose a Singapore cash back card that fits your needs, use it wisely, and watch your savings grow.

For expert recommendations on the best services, products, and lifestyle choices in Singapore, visit TopinSingapore.sg which is your ultimate guide to the best in the city!

Take the first step to online visibility in Singapore. List Your Business — it’s fast and easy.

The best cashback credit card Singapore depends on your spending habits.

Yes! Many category-based cashback cards in Singapore offer 5% or more on selected spending. Examples:

Yes, several flat-rate and category-based cashback cards offer 3% cashback or higher. Examples:

The 2/3/4 rule is a guideline for applying for new credit cards without hurting your credit score. It means:

Applying for too many cards too quickly can lower your credit score and make it harder to get approvals.

Most banks in Singapore require a minimum annual income to qualify for a credit card. The general requirement is:

However, some premium credit cards require higher incomes (e.g., $120,000 per year for luxury cards).

Best Bank Credit Card Offers: Top Deals & Rewards 2025

Stay connected and receive updates directly in your inbox

Showcasing Singapore's top companies for quality services and trusted brands. Get listed with us!